About interpolating yield curves

Financial instruments can have any monthly term, so yield curves are interpolated to provide the basis for calculations.

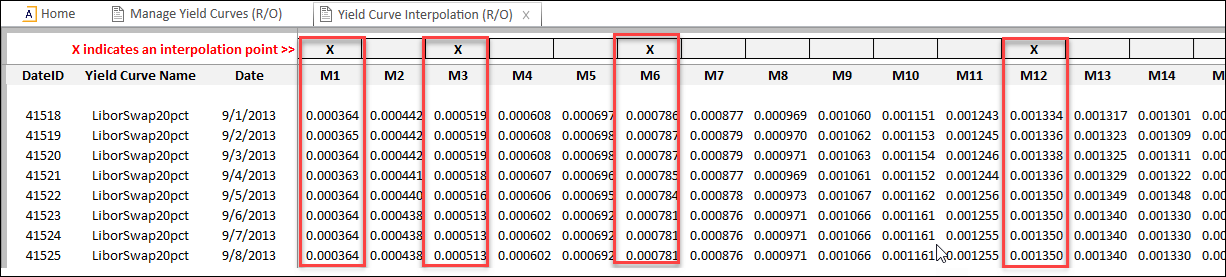

After loading the historical yield curve data, you can interpolate the yield curve rates. Interpolating yield curve rates fills in all terms between the historical yield curve terms. Only fields in between the entered yield curve points are calculated, and only days with no entered rates are created by the interpolation engine. The results are a straight-line interpolated monthly progression of rates between observed rates entered into the yield curve

The Yield Curve Interpolation utility can interpolate the yield curve for a single month of yield curve data, or it can process multiple months of yield curve history as a batch.

FTP currently uses a linear interpolation method. Yield curves interpolated by methods other than linear interpolation need to be generated with a custom utility or generated outside the Axiom system and then loaded into Axiom using a custom yield curve import.

IMPORTANT: Do not use the interpolation utility to process a custom curve that uses a non-linear interpolation method.

NOTE: If a yield curve name exists in the YieldCurve table but not in the YieldCurveSettings table, all utilities, including the Yield Curve Interpolation utility, ignore it. Therefore, all custom curves, as mentioned previously, must be entered in the Yield Curve Settings worksheet of the Manage Yield Curves utility, and provision made to skip interpolation. You can do this by clearing the check box for the interpolation task on the Process FTP page and processing interpolation for other curves manually or creating a custom filter for the Task.

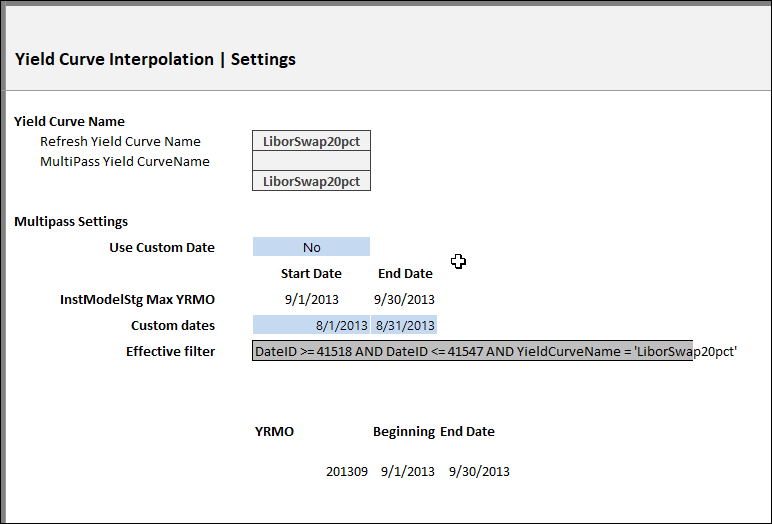

Settings tab of the Yield Curve Interpolation utility

The utility uses the YieldCurveSettings table data to populate the interpolation points on the Interpolate sheet.

Example of yield curve interpolation results

TIP: You can run the interpolation as a standalone task or as part of the main FTP processing sequence.